A Tradition Older Than Banks

Long before credit cards, savings accounts, or financial apps existed, communities across Africa figured out a simple answer to a common problem: how do ordinary people save money and get access to capital when they need it?

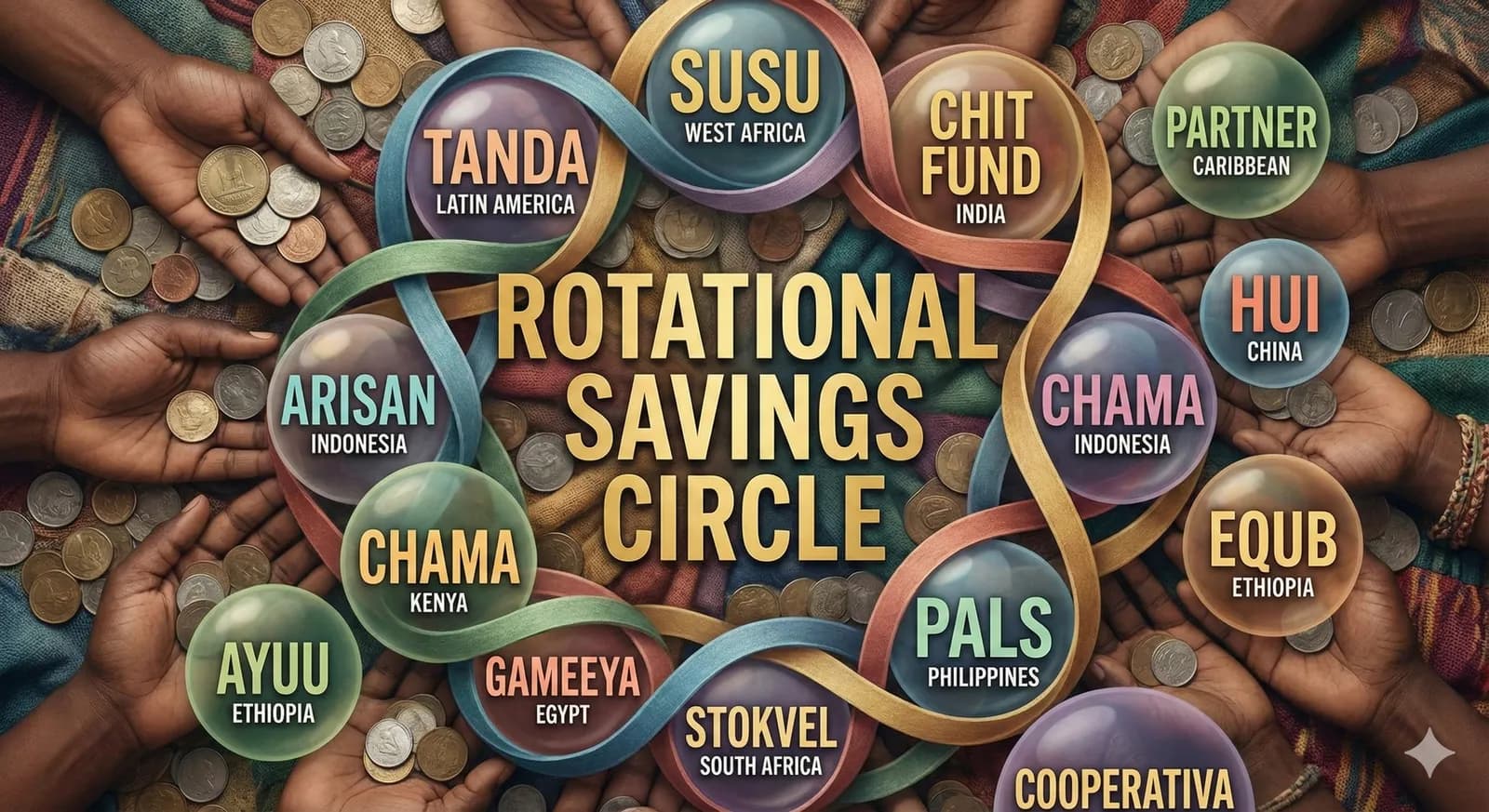

They called it Susu: a rotating savings and credit association (ROSCA) that has helped families build homes, start businesses, and reach financial goals for over 500 years.

The Origins of Susu

The word "Susu" comes from the Yoruba language of Nigeria. It means "to save money little by little." The practice most likely started in West Africa, where it became a normal part of community life.

How It Spread

From West Africa, Susu traveled with people:

- To the Caribbean with the African diaspora, where it is called "Partner" in Jamaica and "Sou-Sou" in Trinidad

- To South America as "Tandas" or "San"

- To Asia where similar systems grew independently: "Chit Funds" in India, "Hui" in China

- To the United States with immigrant communities who brought the tradition with them

The names are different. The idea is the same: people helping people save.

How Traditional Susu Works

How it works

Members contribute together and one person receives the full payout in turn.

This is the core rotating-circle model behind traditional susu savings.

The appeal of Susu is how simple it is:

The Basic Structure

- Form a Group: A trusted group of people (often 10-12) comes together

- Set the Terms: Everyone agrees on a contribution amount and frequency (weekly or monthly)

- Collect the Pot: Each period, all members put in their share

- Distribute: One member receives the entire pot

- Rotate: Members take turns until everyone has received their payout

A Real Example

Take a Susu with 10 members, each contributing $200 monthly:

- Month 1: $2,000 collected, Member A gets the pot

- Month 2: $2,000 collected, Member B gets the pot

- Month 3: $2,000 collected, Member C gets the pot

- ...continues until...

- Month 10: $2,000 collected, Member J gets the pot

When it is done, everyone has saved $2,000. No interest charged. No fees paid.

Why Susu Worked (And Still Works)

Built-In Accountability

When your neighbors, coworkers, or family members are counting on your contribution, you find a way to pay. Social pressure works in your favor here: it is harder to skip a payment or spend impulsively when other people are involved.

Access to Lump Sums

In traditional economies without banks, saving enough for a major purchase on your own was extremely difficult. Susu let people access larger amounts through collective effort.

No Interest or Debt

Unlike loans, Susu does not put members in debt. You receive exactly what you contribute. For communities that avoid interest, whether for religious or practical reasons, this was a big deal.

Community Building

Susu meetings often doubled as social gatherings. The trust built through successful cycles carried over into other parts of life: business partnerships, family support, community leadership.

The Role of the "Susu Collector"

In traditional West African Susu, a trusted person called the Susu Collector had a specific job:

- Daily Visits: Collectors visited market vendors and workers every day to pick up small amounts

- Safekeeping: They held the money until the end of the month

- Distribution: They returned savings to each saver, sometimes keeping one day's worth as their fee

- Trust: Their reputation was everything. A dishonest collector would not last long

This daily collection model worked well for people who had a hard time saving on their own. Small amounts added up into real savings.

Susu in the Modern World

Today's Susu looks different from the original, but the core principles are the same:

What Has Changed

- Digital Payments: Mobile apps replace in-person collections

- Global Reach: Members can be on different continents, not just in the same village

- Verification Systems: Technology helps check member trustworthiness

- Automatic Reminders: No more forgetting contribution day

What Has Not Changed

- Trust-Based: Relationships still matter

- Interest-Free: No riba, no usury, no exploitation

- Community-Powered: Success comes from everyone committing

- Life-Changing: Access to lump sums still makes a real difference in people's lives

Who Uses Susu Today?

Immigrant Communities

First-generation immigrants often turn to Susu when traditional banking feels inaccessible or unfamiliar. It connects them to their heritage while helping them get financially stable in a new country.

Religious Communities

For Muslims following Islamic finance principles (avoiding riba/interest), Susu is a halal alternative. For others, it fits with beliefs about community support and staying away from exploitative debt.

Young Professionals

A new generation is picking up Susu as a way to save for down payments, weddings, or business ventures together with friends who keep them accountable.

Underbanked Populations

People who lack access to traditional banking, whether because of credit history, documentation requirements, or personal preference, find Susu to be a reliable way to save and access capital.

Common Questions About Susu

Is Susu legal?

Yes. ROSCAs like Susu are legal informal savings arrangements between consenting adults. They are not regulated like banks, which is why trust between members matters so much.

What if someone does not pay?

This is the main risk. Traditional circles rely on social pressure and reputation. Modern platforms like Susu add verification and tracking to reduce the chance of this happening.

Who goes first?

Groups handle this differently:

- Lottery: Random drawing determines order

- Need-Based: Members with urgent needs go early

- Auction: Members bid for early positions

- Fixed: Order stays the same each cycle

Is it like a loan?

Not exactly. There is no interest. If you receive your payout early, you keep contributing until the cycle ends. If you receive it late, you have essentially saved the full amount before getting it back.

Starting Your Own Susu

Whether you use a digital platform or organize it yourself, here is how to begin:

1. Gather Your Circle

Choose people you trust: family, close friends, coworkers, or community members with similar values and financial situations.

2. Set Clear Terms

Agree on:

- Contribution amount (make sure everyone can afford it)

- Frequency (weekly, bi-weekly, or monthly)

- Payout order (how will you decide?)

- What happens if someone misses a payment

3. Document Everything

Even among people you trust completely, written agreements prevent misunderstandings. Write down:

- Members' names and contact information

- Contribution schedule

- Payout order

- Rules for late payments

4. Choose Your Method

- Traditional: In-person meetings, cash contributions

- Digital: Apps like Susu handle payments, tracking, and reminders

- Hybrid: Meet in person but use digital payments

5. Celebrate Together

Do not just exchange money. Celebrate each payout. Those moments build the community that makes Susu worth doing.

The Future of Susu

As digital technology makes Susu more accessible, millions more people are finding (or rediscovering) this old practice. What started in West African markets now happens in WhatsApp groups and mobile apps around the world.

But the technology is just a tool. The real power of Susu has not changed in 500 years: people trusting each other, supporting each other, and reaching goals together that they could not reach alone.

Want to try this for yourself? Download Susu and join the millions of people building financial freedom the way communities have done for centuries.